- | F. A. Hayek Program F. A. Hayek Program

- | Expert Commentary Expert Commentary

- |

Should We Be Worried about High Inflation from the Fed’s Recent Money-Printing?

Much of my research over the years has concerned the operating characteristics of banking and monetary regimes (free banking with a specie standard) different from the one we currently have (central banking on a fiat standard). Here I want to discuss what we can expect from the current system in the months and years ahead. Many observers are understandably worried that the Federal Reserve System’s rapid expansion of the money supply during recent months, as part of an effort to dampen the COVID-19 recession, will soon bring high inflation. “Money printer go brrr,” warns a meme popular among Bitcoin proponents.

Under the impact of unprecedented bond-purchase and lending programs by the Federal Reserve, US money aggregates have been growing at what normally would be alarming rates. As of mid-July, the M1 measure of money held by the public was up 31.6 percent over six months earlier. If the Fed were to continue that M1 growth at that rate for another six months, the money stock would grow 72.7 percent over the year. The broader M2 aggregate has likewise turned upward, though not quite as sharply. Mid-July’s figure was up 19.7 percent over mid-January’s, which would compound to 43.2 percent annual growth.

Fig. 1. Due to Fed monetary policy, the M1 Money Stock has risen rapidly in 2020. Source: Board of Governors of the Federal Reserve System (US), retrieved from FRED, Federal Reserve Bank of St. Louis

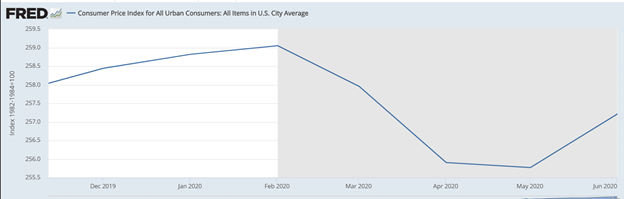

Back in April, prominent inflation warnings were issued by Martin Hutchinson in the National Review[1] and by Tim Congdon in The Wall Street Journal[2], as skeptically noted by George Selgin.[3] In a Washington Post article, Heather Long quoted David Kelly, chief global strategist at JPMorgan Funds, wondering “how far Washington can go in issuing and monetizing debt before everyone pays a price in terms of higher interest rates, higher taxes and higher inflation.”[4] These fears moved to the back burner with March, April, and May actually recording deflation in the US. The month-over-month changes in the Urban Consumer Price Index were -0.4 percent, -0.8 percent, and -0.05 percent, respectively.[5] June saw an uptick in prices, however, with the CPI-U rising 0.6 percent over the previous month, a rate that annualizes to 8.7 percent per year. In July, with gold prices rising, inflation warnings returned. Bloomberg reporters noted “a nervous vibe that has infiltrated the market this month: Investors worried that this money-printing will trigger inflation in years ahead.”[6]

Fig. 2. Despite monetary expansion, the CPI-U price index has fallen in 2020. Source: U.S. Bureau of Labor Statistics, retrieved from FRED, Federal Reserve Bank of St. Louis

Still, the CPI-U is down 0.6 percent since the start of 2020. Why has inflation failed to keep up with money growth? Is it only because there is a “long and variable lag” between money growth and a corresponding rise in the CPI? Will we have double-digit inflation during the second half of 2020?

I do not think double-digit inflation is likely, although future Fed policy remains to be seen. The current surge in money growth will not bring corresponding price inflation so long as it continues to only offset a contemporary drop in spending due to shuttered businesses and household isolation associated with the COVID-19 pandemic. (Based on Google data, William Luther estimates that about three-fourths of reduced mobility has been voluntary, having preceded the issuing of stay-at-home orders by state governments, and the remaining one-fourth is involuntary.)[7] Households have been passively absorbing the money balances created by the Fed for two reasons: (1) uncertainty about economic prospects (the ratio of money balances to spending also rose dramatically during the recession in 2008–2009), and (2) the pandemic-associated drop in shopping outside the home.

The end of stay-at-home orders and reduction of self-isolation will naturally result in a resumption of normal spending, although nobody knows to what degree or how soon the rebound will occur. To avoid double-digit inflation as spending resumes, the Fed will have to reverse its current expansionary policy and begin to withdraw no-longer-wanted money balances from the economy. Getting the timing just right will be impossible. Just as there is no historical guide to such a drop in spending due to pandemic isolation, there is no guide to the speed of resumption.

It follows that the Fed can be expected to miss its self-adopted two percent annual inflation target. For the first half of 2020, it has missed its target on the low side by a margin of 2.6 percentage points. Presumably the Fed is trying to correct that undershoot. During some later period, it may well miss the inflation target on the high side (hence the market surge in dollar-inflation hedges like gold and Bitcoin). The Fed could avoid inflation misses only if it had perfect foresight, and could correctly calibrate and time its quantitative easing and later tightening to exactly offset the slump and the later revival in spending (alternatively stated, hoarding and dishoarding of money balances). The Fed, like everyone else, does not have perfect foresight, so to some extent errors are unavoidable.

As my Mercatus colleagues David Beckworth[8] and Scott Sumner[9] have pointed out in analyses of the Fed’s responses to the current crisis and to the Great Recession, the Fed has tended to make two avoidable errors: (1) when a shock hits and forecasts change, it adjusts monetary policy too slowly to return to its own target path, and (2) in the face of a negative supply shock, the Fed’s pursuit of an inflation target requires monetary tightening which, by contrast to a nominal spending target, worsens macroeconomic disequilibrium in a world of nominal rigidities.

In other words: in a fiat money regime, previously established nominal wages, rents, and debts are no longer market-clearing when nominal income (NGDP) grows less than expected. Fed conformity to an inflation (rather than nominal income) target creates avoidable discoordination in the face of a negative real shock because it compels nominal income to decline below its established trend. The first quarter of 2020 was bad enough (-0.9 percent NGDP growth when +1.0 percent quarterly growth had been the trend). Preliminary figures for the second quarter are far worse: a whopping -10 percent growth (not seasonally adjusted). The monetary policymakers on the Federal Open Market Committee (FOMC) even by their own forecasts are currently not expanding enough to restore NGDP growth. The FOMC’s June 2020 median forecast is for -5.3 percent nominal GDP growth over 2020 as a whole.

Unprecedented Lending Operations

In response to COVID-19, as Ben Bernanke and Janet Yellen have dryly noted, “The Fed also has been active beyond monetary policy.”[10] Accordingly, there are other reasons to be concerned about the Fed’s current policies. The first reason is the unprecedented set of lending and bond-purchasing operations through which the Fed is expanding the stock of base money. These innovations show up on the asset side rather than the liability side of the Fed’s balance sheet. The second reason, discussed in the next section, is that Congress, using the Fed for political ends, as demonstrated by the Fed’s involvement in pandemic policy, has implications for longer-term inflation.

To quote one part of Bernanke and Yellen’s description of the Fed’s expanded role:

… the Federal Reserve, with the support of the Congress and the Treasury, has also served during the current crisis as a lender of last resort to the non-financial sector, backstopping key credit markets facing the prospect of severe disruption from the pandemic. To take on this role, the Fed invoked its emergency lending powers under Section 13(3) of the Federal Reserve Act. Since those powers require that the Fed’s lending be well secured, it has had to rely on funds appropriated by the Congress and allocated by the Treasury to cover possible losses. Using these authorities, the Fed revived financial crisis-era facilities to stabilize commercial paper and asset-backed securities markets. Going beyond the financial crisis playbook, the Fed has also added new facilities to lend to corporations and state and local governments and to buy outstanding corporate bonds.[11]

Allocating taxpayer money to officially chosen recipients — by directly lending to corporations or to state and local governments or purchasing their bonds — has traditionally been considered fiscal policy, and the exclusive prerogative of Congress. Scott Burns and I have described how the Fed improperly pursued credit allocation in its response to the Great Recession.[12] Current policy embodied in Congressional and self-initiated expansions of the Fed’s credit-granting activities, as Alexander W. Salter has warned in several pieces, goes even farther in the wrong direction.[13] The Fed has seldom resisted political pressure, as Daniel J. Smith and Peter J. Boettke have emphasized. [14] Credit allocation further politicizes the Fed, opening the door to cronyism (or “rent-seeking”[15]) and the associated waste of resources on lobbying battles. Political credit allocation breeds moral hazard. Most importantly, it impairs long-term economic growth by redirecting loanable funds toward politically-connected existing firms at the expense of the most promising new firms.

The Long-run Inflation Outlook

If the Federal Reserve remains committed to keeping inflation near two percent, it will need to reverse the growth of M1 as the coronavirus pandemic recedes, and as the pandemic-related surge in the real demand to hold money recedes with it. But if the Fed is beholden to Congress, for how long will the Fed remain committed to a target of two percent?

Economists Antony Davies and James R. Harrigan write that “the Federal Reserve has reached a point wherein it has little choice but to monetize federal deficits. Sooner or later, we will all pay the price in the form of massive inflation.”[16] Although “sooner or later” is open-ended as to timing, Davies and Harrigan suggest that ongoing larger deficits will compel an ongoing higher rate of money-printing and thus “will give us sustained and significant inflation.”[17] How solid are those linkages, actually?

The current fiscal picture is certainly alarming. In its “Monthly Budget Review for June 2020” the Congressional Budget Office reported the following figures:

The federal budget deficit was $2.7 trillion in the first nine months of fiscal year 2020, CBO estimates, $2.0 trillion more than the deficit recorded during the same period last year…. Revenues were 13 percent lower and outlays were 49 percent higher through June 2020 than during the same nine-month period in fiscal year 2019.[18]

If the budget deficit for the full fiscal year of 2020 (ending September 30th) comes in at $3.7 trillion, as projected, that will be an incredible 19 percent of 2020’s projected GDP ($19.4 trillion). To finance the extraordinarily large deficit, the US Treasury has been issuing an extraordinarily large volume of bonds. At the current rate, the ratio of Treasury debt held by the public to GDP will soon surpass the World War II-level of 106 percent.

The Fed’s heavy bond-buying of 2020 has thus corresponded with a period of heavy US Treasury bond-issuing. Is that correspondence merely coincidental, or has the Fed been accommodating the Treasury’s borrowing to keep Treasury bond prices high and their yields remarkably low? Brookings Institution Fellow David Wessel notes that “between mid-March and late June 2020,” the Fed purchased more than half of the Treasury bonds issued: about $1.6 trillion out of $2.9 trillion.[19]

It might be argued that the linkage between Treasury deficits and Fed money-printing is historically weak. And now that the Fed pays interest on the bank reserves it creates when it buys Treasuries at a rate comparable to Treasury bond yields, there is almost no additional profit (seigniorage) to the Treasury from the Fed’s monetizing of more debt. This argument focuses entirely on annual flows, however, and ignores the influence of the mounting stock of Treasury debt. The larger the stock of dollar-denominated debt, the more tempting is surprise inflation as a way to pay it back cheaply.

Whether the long-term inflation outlook remains about two percent, then, depends on whether the Treasury can continue to roll over its debt at low interest rates, as it does now, keeping its annual debt service from growing as a share of the federal budget, without needing the partial debt repudiation from inflation higher than two percent. If high-deficit fiscal trends continue, saturating the market for US Treasury debt to the point that debt service consumes a growing share of the budget, the temptation to inflate will build. Keeping the inflation rate from rising will eventually require an explicit Congressional commitment to restraining growth in the ratio of public debt to GDP, or some more fundamental reform of the monetary system — a rule or an institutional change — that explicitly limits or eliminates the Fed’s ability to expand the stock of money.

Read More:

- Paul Dragos Aligica, Peter J. Boettke, and Vlad Tarko. Public Governance and the Classical-Liberal Perspective: Political Economy Foundations (Oxford, England: Oxford University Press, 2019).

- Ekkehard A. Köhler, Viktor J. Vanberg, and Lawrence H. White (Editors), Renewing the Search for a Monetary Constitution: Reforming Government’s Role in the Monetary System (Washington, DC: Cato Institute, 2015).

- Richard E. Wagner, Public Debt as a Form of Public Finance (Cambridge, England: Cambridge University Press, 2019).

- Lawrence H. White, The Clash of Economic Ideas: The Great Policy Debates and Experiments of the Last Hundred Years (New York: Cambridge University Press, 2012).

- Lawrence H. White, The Theory of Monetary Institutions (Malden, MA: Blackwell Publishers, 1999).

Learn more about the Hayek Program and submit a research proposal to get involved.

More Commentary on the COVID-19 Pandemic:

- Coming Back from COVID-19: Lessons in Entrepreneurship from Disaster Recovery Research

- Reassessing the Notion of Work During the COVID-19 Pandemic

- The European Union’s Governance System and the COVID-19 Pandemic

- Doing Bad by Doing Good during the COVID-19 Pandemic

- How Can Economics Help Us to Better Understand COVID-19?

- Native American Reservations and COVID-19: Understanding the Plight of Reservations in the Current Pandemic

- Polycentricity Amidst a Pandemic

- Inequality and Surveillance During the COVID-19 Pandemic

- Market Regulation and COVID-19 Response: Pain, Change, and Opportunity

Author:

Lawrence H. White is a professor of economics at George Mason University and a distinguished senior fellow for the F. A. Hayek Program for Advanced Study in Philosophy, Politics, and Economics at the Mercatus Center at George Mason University.

Notes:

[1] Martin Hutchinson, “The Coronavirus Economy Will Bring Inflation,” National Review, April 23, 2020, https://www.nationalreview.com/2020/04/the-coronavirus-economy-will-bring-inflation/.

[2] Tim Congdon, “Get Ready for the Return of Inflation,” The Wall Street Journal, April 23, 2020, https://www.wsj.com/articles/get-ready-for-the-return-of-inflation-11587659836.

[3] George Selgin, “Return of the Inflation Mongers,” Alt-M, April 27, 2020, https://www.alt-m.org/2020/04/27/return-of-the-inflation-mongers/.

[4] Heather Long, “The Federal Reserve Has Pumped $2.3 Trillion into the U.S. Economy. It’s Just Getting Started,” The Washington Post, April 29 2020, https://www.washingtonpost.com/business/2020/04/29/federal-reserve-has-pumped-23-trillion-into-us-economy-its-just-getting-started/.

[5] Bureau of Labor Statistics, “Consumer Price Index — June 2020,” July 14, 2020, https://www.bls.gov/news.release/pdf/cpi.pdf.

[6] John Ainger and Liz McCormick, “Goldman Warns the Dollar’s Grip on Global Markets Might Be Over,” BloombergQuist, July 28, 2020, https://www.bloombergquint.com/markets/goldman-warns-dollar-s-role-as-world-reserve-currency-is-at-risk.

[7] William Luther, “Behavioral and Policy Responses to COVID-19: Evidence from Google Mobility Data on State-Level Stay-at-Home Orders,” AIER Sound Money Project Working Paper №2020–06, May 11, 2020, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3596551.

[8] David Beckworth, “Making Up Is Not So Hard to Do,” National Review, July 28, 2020, https://www.nationalreview.com/2020/07/federal-reserve-coronavirus-crisis-highlights-central-banks-limited-ability-to-respond-economic-disasters/.

[9] Scott Sumner, “Re-Targeting the Fed,” National Affairs, Fall 2011, https://www.nationalaffairs.com/publications/detail/re-targeting-the-fed.

[10] Ben Bernanke and Janet Yellen, “Former Fed Chairs Bernanke and Yellen Testified on COVID-19 and Response to Economic Crisis,” The Brookings Institution July 17, 2020, https://www.brookings.edu/blog/up-front/2020/07/17/former-fed-chairs-bernanke-and-yellen-testified-on-covid-19-and-response-to-economic-crisis/.

[11] Bernanke and Yellen (2020).

[12] Scott A. Burns and Lawrence H. White, “Political Economy of the Fed’s Unconventional Monetary and Credit Policies,” Cato Journal, Spring/Summer 2019, https://www.cato.org/cato-journal/springsummer-2019/political-economy-feds-unconventional-monetary-credit-policies.

[13] Alexander W. Salter, “The Fed’s Creeping Mandate Is Cause for Concern,” RealClearMarkets, July 8, 2020, https://www.realclearmarkets.com/articles/2020/07/08/the_feds_creeping_mandate_is_cause_for_concern_498363.html; Alexander W. Salter, “COVID-19 Made the Federal Reserve Sick,” American Institute for Economic Research, June 24, 2020, https://www.aier.org/article/covid-19-made-the-federal-reserve-sick/.

[14] Peter J. Boettke and Daniel J. Smith, “An Episodic History of Modern Fed Independence,” The Independent Review, Summer 2015, https://www.independent.org/pdf/tir/tir_20_01_08_smith.pdf; See also their forthcoming book with Alexander W. Salter: Money and the Rule of Law.

[15] David R. Henderson, “Rent Seeking,” Econlib, Accessed August 3, 2020, https://www.econlib.org/library/Enc/RentSeeking.html.

[16] Antony Davies and James R. Harrigan, “Massive Inflation May Be Coming, Because the US Government Has Cornered Itself into a Fiscal End Game,” Foundation for Economic Education, May 21, 2020, https://fee.org/articles/massive-inflation-may-be-coming-because-the-us-government-has-cornered-itself-into-a-fiscal-end-game/.

[17] Davies and Harrigan (2020).

[18] Congressional Budget Office, “Monthly Budget Review for June 2020,” July 8, 2020, https://www.cbo.gov/publication/56458.

[19] David Wessel, “How Worried Should You Be About the Federal Deficit and Debt?,” The Brookings Institution, July 8, 2020, https://www.brookings.edu/policy2020/votervital/how-worried-should-you-be-about-the-federal-deficit-and-debt/.

Additional details

Read the original article at The Vienna Circle.

Related Content

- | F. A. Hayek Program F. A. Hayek Program

- | Expert Commentary Expert Commentary

How Can Economics Enable Us to Better Understand COVID-19?

- | F. A. Hayek Program F. A. Hayek Program

- | Expert Commentary Expert Commentary

Doing Bad by Doing Good during the COVID-19 Pandemic

- | F. A. Hayek Program F. A. Hayek Program

- | Expert Commentary Expert Commentary

The European Union’s Governance System and the COVID-19 Pandemic